New Developments in Longevity Risk Transfer Market

Macquarie University has released a report focused on measuring longevity basis risk in realistic scenarios as part of an ongoing research project sponsored by the Life and Longevity Markets Association (LLMA) and Institute and Faculty of Actuaries (IFoA). Here, Actuarial Professors at Macquarie Uni, Jackie Li and Leonie Tickle, explain their findings.

While most longevity transactions so far have been customised in nature, index-based solutions and standardised products could draw more interest from financial entities both inside and outside the insurance industry.

They have much potential in providing effective risk management at lower costs and significant capital savings.

Some of the products in Table 2 (below) have already been issued and tested in practice, with different levels of success. However, the potential mismatch between the hedging instrument and the pension or annuity portfolio being hedged leads to longevity basis risk.

The research project sponsored by IFoA and the LLMA aims to address this problem.

Phase 1 of the project was completed by Cass Business School and Hymans Robertson LLP in December 2014, in which a decision tree framework was developed as a practical guide on how to select a two-population mortality model (Haberman et al., Longevity Basis Risk: A Methodology for Assessing Basis Risk, 2014, IFoA).

Phase 2 of the project, focusing on measuring longevity basis risk in realistic scenarios under practical circumstances, was completed by Macquarie University recently, with the report released in November 2017 (Li et al., Assessing Basis Risk for Longevity Transactions – Phase 2, 2017, IFoA).

There is a huge potential for the life market to continue to grow. When global economic conditions improve, hedging instruments become more widely affordable, financial institutions offer more innovative products, and pension plans sponsors and market investors have a better understanding of longevity risk transfer, the life market will have a great chance to flourish.

Actuaries working in life insurance and superannuation are encouraged to keep up-to-date with the latest development in this area.

A broader perspective

Continual improvement in mortality is a worldwide phenomenon. While it is certainly something to celebrate for human beings, it imposes a significant challenge to pension plan sponsors and annuity providers. “Longevity risk” is the risk that pension plans or annuity portfolios pay more than expected because of unanticipated mortality decline. This risk is composed of systematic longevity risk and non-systematic longevity risk. The latter risk can usually be reduced by increasing the portfolio size, but the former cannot be mitigated in the same way. In general, governments and financial institutions are very cautious about taking on too much longevity risk.

Tackling longevity risk

Currently, there are three ways for financial institutions to tackle longevity risk:

1). Traditional insurance and reinsurance, in which the risk is passed on to an insurer or reinsurer after paying a premium. For example, an insurer can purchase a reinsurance contract to hedge away the risk, or a pension plan can buy annuities from an insurer to cover the risk for its members. (A recent alternative is the group self-annuitisation approaches.)

2). Natural hedging, which exploits the opposite movements between the values of annuities and life insurances (Li and Haberman, Insurance: Mathematics and Economics, 2015). This diversification approach may be viable for larger institutions with the financial resources and structure to sell both kinds of products. It may also be implemented by using a customised mortality swap to build an external hedge between two separate parties who have life insurances and annuities respectively on their books.

3.) Capital market solutions, including insurance securitisation, mortality- or longevity-linked securities, and derivatives. This method has seen much development in the UK in recent years. Insurance securitisation means securitising a class of business as a complex bundle into highly structured securities for sale to market investors. Some popular de-risking solutions such as buy-ins, buy-outs, and longevity swaps are also bespoke transactions for hedging specific portfolios.

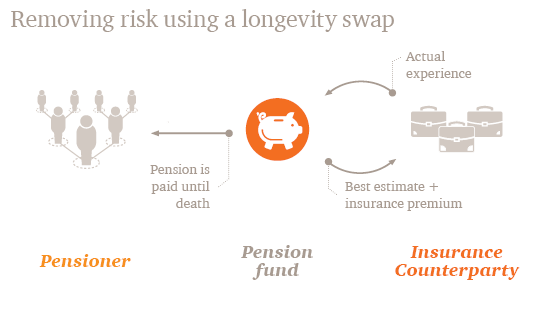

Table 1 shows a few examples of the recent longevity swaps transactions (www.artemis.bm), and Figure 1 demonstrates how a bespoke longevity swap works.. Figure 2 (Li et al., Assessing Basis Risk for Longevity Transactions – Phase 2, 2017) illustrates that the UK de-risking market has grown in size significantly since 2007.

On the other hand, standardised mortality- or longevity-linked securities and derivatives have their cash flows linked to a selected reference or index population, instead of the population underlying the portfolio to be hedged. There would then be a potential mismatch between the hedging tool and the portfolio, in terms of demographic differences. Moreover, a small portfolio would have high sampling variability, which makes it more likely to deviate from the index population. Also, the payoff structures would often be different between the hedging instrument and the portfolio being hedged. All these discrepancies are referred to as longevity basis risk, and are under intense research. The major types of standardised, index-based securities proposed in the longevity literature are listed in Table 2.

Table 1 Recent longevity swaps transactions

Figure 1 A bespoke longevity swap

*Graph source: PWC

Figure 2 Buy-ins, buy-outs, and longevity swaps volumes from 2007 to 2015 in UK

Table 2 Index-based longevity-linked and mortality-linked securities

The Life and Longevity Markets Association (LLMA) was established in the UK by several global insurers, reinsurers, and investment banks in 2010 to develop a liquid ‘life market’, which serves as a platform for insurers, reinsurers, and market investors to trade various longevity- and mortality-linked assets and liabilities. Market investors may accept longevity risk from insurers and pension plans in exchange for appropriate risk-adjusted returns. Some may want to diversify across a new market sector of longevity, which is arguably uncorrelated with traditional asset classes. Those who have life insurances on their books may want to take on longevity exposures to offset their own risks. Since then, there have been many interesting and innovative developments in the life market (Tan et al., Insurance: Mathematics and Economics, 2015).

CPD: Actuaries Institute Members can claim two CPD points for every hour of reading articles on Actuaries Digital.

{kind=link}