Financial Risks of Climate Change: Piranhas or Red Herrings?

The world’s leading authority on climate change, the Intergovernmental Panel on Climate Change (IPCC), has long warned that unless urgent action is taken, we are on course to experience irreversible and catastrophic environmental consequences of global warming under a range of plausible physical climate scenarios by the end of this century and beyond.

More recently, central banks and financial regulators have posited that climate change – both through its physical impacts as well as efforts to transition to a greener future – poses a threat to the stability of the global financial system, sparking a race to better understand and quantify climate impacts within the financial industry. This has led to a rise in the use of climate scenarios within stress tests conducted by regulators across the globe.

Curiously, the preliminary findings portray a very different and benign picture when juxtaposed against IPCC findings, giving rise to the current debate around whether climate scenarios have been used appropriately and whether stress testing is indeed robust and decision-useful.

Acknowledging that this area is an emerging discipline, it is instructive that the null hypothesis of widespread financial stress associated with future climate change remains unsupported by the multi-jurisdictional findings to date.

As such, this article aims to shed light on key reasons for this disconnect by first contextualising the application of climate scenarios within stress tests before highlighting methodological challenges in the development of physical and transition risk scenarios.

Traditional Stress Tests vs Climate Scenarios

As climate risks typically materialise over a far longer period compared to non-climate-induced macroeconomic shocks and involve the introduction of climate variables that are beyond the socioeconomic realm, traditional stress testing approaches and frameworks have been adapted to cater for these fundamental differences.

Before critically assessing the methodology of climate scenarios, it is important to appreciate the way climate scenarios have been used within stress tests as this, in part, explains why results have not been as severe as that of traditional non-climate macro-prudential exercises.

Firstly, a typical traditional, non-climate scenario often features pathways that resemble a financial crisis. A severe and long-lasting recession featuring a fall in GDP, unemployment rises in the real economy and turmoil that ensues within the financial markets with spikes in risk premia and sharp share price declines.

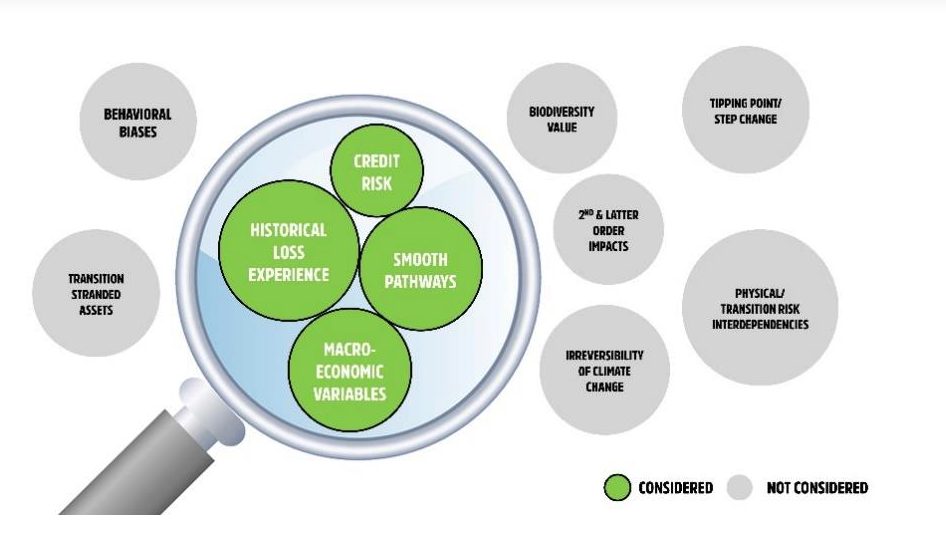

Climate scenarios to date simply do not produce this level of severity and instead feature smooth macroeconomic pathways.

The second important distinction is the assumption of a recovery pathway within traditional scenarios. Most economic variables assume a recovery pathway (i.e., GDP/unemployment tends to be V/tent-shaped) following a shock event. But this may not hold for climate risk, particularly physical climate risk as irreversible tipping points are crossed.

Rather than simulate a shock event followed by recovery, climate scenarios by design will duly arrive at a new normal or baseline, with the deviation from ‘non-climate impacted’ trajectories as well as stranded assets (i.e., infrastructure impacted by sea level rise) treated as climate-related costs.

Lastly, traditional stress testing regimes tend to have a narrow focus on financial shock events – which may be too restrictive to capture the wide-ranging impacts and uncertain loss pathways of climate risk.

Historically, not every recession has necessarily caused or followed a financial crisis. This is because financial crises are fundamentally triggered through the mispricing or repricing of financial assets, combined with insufficient capital of major financial actors such as banks to absorb the shock.

The COVID-19 pandemic, which saw a much larger drop of GDP compared to the 2008 Global Financial Crisis (GFC), is a good example of the above distinction. Conversely, an example of a potentially developing crisis would be the very recent failure of Silicon Valley Bank – hardly a systemic financial institution by any measure – but yet, we are already starting to see spillover impacts such as a broader bank run on similar smaller regional banks, potential interruption of central bank rate policy, as well as foreign exchange (FX) impacts.

While there has not been any conclusive evidence to date, physical climate risk is arguably more likely to manifest in systemic damage to the real economy before ensuing financial crises – further discussed in the following sections.

Transition risk

In 2020, the Network for Greening the Financial System (NGFS) produced the first set of climate scenarios derived from three different integrated assessment models (IAMs): REMIND-MagPie, MESSAGE-GLOBIOM and GCAM.

All of these scenarios and their respective IAMs are based on the shared socioeconomic pathways 2 (SSP2), which prescribes common assumptions on population, economic development, institutional strength and technological progress. The publication of these scenarios proved a challenge to scenario economists and modellers at financial institutions on several fronts.

As a start, the number of variables is a multiple of what traditional stress testing has been using. For any specific region or country, there are more than 700 specific variable concepts across six scenarios, three modelling systems and several regions and countries.

The first NGFS IAM vintage had a total of more than 800,000 variable paths. Then again, out of this large IAM data set, there were only a limited number of variables that financial institutions would have mapped to their traditional set of variables at the time. Beyond real GDP and a generic crude oil price, most variable concepts were alien to risk managers that were erstwhile familiar only with macro-financial variables.

It is important to point out that the leading research institutes did not consider the macro-financial impact, such as frictions in credit markets, the dynamics of the yield curve nor the impact on foreign exchange. Their initial objective was to estimate future emissions and possible pathways to mitigate climate change. With some of these models there is no discounting, markets clear and agents have perfect foresight. None of these assumptions are necessarily wrong to fulfil their initial objective amongst non-financial policy-makers, but the issue lies with its simple extension to the financial landscape that proves problematic, and the remainder of this section will explore some of these challenges in more detail.

First, climate transition scenarios are unable to produce acute financial shocks by design mainly because key macro-financial variables are too smooth and do not feature recessions. This is further compounded by modelling time steps of five-year increments that are far too temporally coarse to capture sudden events, particularly compared to traditional stress tests (in the case of Bank of England, quarterly intervals).

However, IAMs can still be helpful to inform climate risk views if attention is focused on other more specific features rather than the key macroeconomic variable paths or ‘red herrings’ for financial institutions. For example, a more liberal interpretation of insights of IAM will lead to consideration not simply of losses but future revenue streams, provoking pertinent questions such as the cessation of investment to the oil/gas industry in the near future, crowding out the impact of large investment cycles on particular industries, or technologies that need to be phased out.

Next, the scenarios, in part owing to its inherent complexity and the primary user base of stress testers, are often misconstrued to represent tail-risk events (scenarios that will occur with a small probability), as well as being static in nature couched in fixed time frames.

In fact, the scenarios were specifically designed to simulate a range of plausible futures – ranging from pathways that achieve net zero on the one hand, or in the case of the so-called ‘hot house’, miss-stated emission targets.

As such, instead of substituting scenarios as proxy stress tests, financial market participants should apply them as a baselines to benchmark their own long-term strategy, where stresses could occur within ANY given scenario. The fixed time frame conundrum refers to the practice common within traditional stress testing to recycle the same scenario – with minor adjustments – as a ‘roll forward’ from the previous year. This is especially problematic for transition risk, due to the speed of transition to different technologies.

For example, one of the most radical transitions of technology involves horse-drawn carriages being substituted by hydrocarbon-fuelled transport such as the internal combustion engine. However, it did not result in widespread stranded asset risk as the transition occurred over almost 100 years. In contrast, IAMs are predicting a transition of fewer than 10 years for a wide-range of industries, which is often shorter than the investment cycle of most capital goods. As such, adopting a ‘roll forward’ fixed time frame approach underestimates the dynamic, rapidly growing risk profile of scenarios. In particular, the Net Zero by 2050 is not a movable target and merely seven-years from now would be the start of the ‘delayed scenario’ which sees far higher carbon pricing and drastic action required to reach net zero.

Lastly, another key reason for artificially mild scenario loss outcomes stems from the fact that IAMs do not explore a disruptive path across technologies and energy transformation.

In these scenarios, market participants perfectly plan, invest and price with just the right amount of energy generated or sufficient demand for biomass. In reality, and as history and behavioural economics have demonstrated time and time again, this is unrealistic.

It is not difficult to imagine that there may be periods when there is insufficient electricity to meet the demands of a growing electric vehicle (EV) sector. In addition, the urgency to develop untested clean technologies may exacerbate herd-mentality and optimism bias, manifesting in the tunnel vision of investors as has occurred in past periods of technological disruptions where investors, creditors and policy-makers collectively failed to detect systemic issues. Given the rapid speed of innovation, not only fossil fuel but renewables may turn into stranded assets as today’s latest solution to energy storage may become obsolete tomorrow.

Physical risk

Historical climate risk and associated loss outcomes have often been offered as an explanation or evidence to support non-severe impacts. However, what this critically misses is that we have not felt the full brunt of elapsed climate change (due to time lags), and that the next hundred years of climate change will look fundamentally different to the last hundred years, even under more optimistic scenarios.

Scientific literature is rich in content exploring regime change and non-linearities in the frequency and severity profile of acute extreme events and thresholds/ step changes/ selected tipping points, compound events and feedbacks. This supports the contention that historical experience may be a poor predictor of future impacts. Additionally, there is also growing inter-connectivity within the global economy and hidden supply chain inter-dependencies that have been laid bare by COVID.

As alluded to earlier in the article, another issue is the framing of loss outcomes in terms of credit, market or liquidity risk that only considers direct losses suffered by financial institutions.

In reality, bank’s may be insulated from physical climate risk by multiple buffers, thus an overt focus on financial loss outcomes masks the wide-ranging impacts of climate to the real economy and society at large. For example, the impacts of acute physical risk to residential mortgage credit risk are modest (especially relative to the GFC) , particularly for a large and geographically well-diversified portfolio buffered by general and lender’s mortgage insurance protection.

Historically, even in instances where insurance is either unaffordable or unavailable, governments have stepped in to provide subsidies through risk pool schemes funded ultimately through the tax-payer or the government’s ability to raise debt. Thus, focusing exclusively on credit loss outcomes risks being lulled into a false sense of security as the collective burden of society is ignored, with banks latently saddled with outsized stranded assets in a future when physical climate risk burden (both due to portfolio growth and climate change influence on extreme weather events) exceeds the insurance sector and government’s cushioning capacity threshold.

Since inaugural climate stress tests around the world have been commissioned, they have yielded modest results for physical risk. Portfolio composition and industry mix aside – these stress tests often use what has emerged as the de-facto ‘industry’ standard for climate scenario analysis methods prescribed by NGFS. Ostensibly to enable comparison between different financial actors to inform investors, it means that scenario views are informed by a limited set of methodologies. In the case of NGFS, the recommended approach to estimating chronic physical risk, as well as the future time period of interest, has an impact on the modelled severity of loss outcomes.

While it has been observed that real GDP per capita and temperature (i.e., hotter countries tend to be poorer) are correlated, the Kalkuhl and Wenz, 2020 methodology prescribed by NGFS focus on central tendency through the use of least squares estimates, as well as being limited to losses (particularly labour and productivity) stemming purely from temperature. Importantly, this disregards the impact of sea level rise and other lesser-known risk factors, such as soil subsidence. There is arguably a further ‘dilution’ of potential impact through the use of annual mean temperature and precipitation on a regional basis.

Furthermore, the lack of consideration of ecosystem services in the advent of biodiversity decline is notable. A more robust estimate taking into account reduced pollinator efficiency (with agriculture and food security consequences), excess carbon release in wildfires, ocean acidification and warming, and impacts to other critical systems will paint a more complete picture of physical risk impact beyond the scope of GDP.

Most stress tests focus on projecting impacts at 2050 time horizon which misses capturing the essence of nonlinearities documented above. Although a distant timeline maybe difficult to reconcile for an industry that has been primarily focused on short term performance, a 2050 view for physical risk renders the exercise limited in utility and is precisely one of the key reasons why IPCC and other scientific bodies use end-of-century projections to inform policy and warn of the devastating impacts of climate inaction.

No consideration for combined physical and transition risk dynamics

Although it is convenient to compartmentalise physical and transition risk neatly into separate buckets (as is the case with existing frameworks), the reality is highly nuanced with significant interdependency between these two broad risk types.

Continuing to treat physical and transition risks as separate within the broader climate risk taxonomy leads to over-simplified scenario outcomes. Ideally, scenarios should not create a false trade-off narrative with less physical risk in a transition scenario. Physical risk will at least be as high in any transition scenario for the next 20 years.

In fact, a direct link between physical and transition risk domains can be found in energy demand projections and the efficacy of renewable energy targets. For example, the severe drought that impacted Europe and China during the northern hemispheric summer of 2022 led to the drying of hydropower (various dams across Europe or the Yangtze in China). As these drought events are projected to worsen in the future, it could force a re-pivot to fossil fuel-driven energy sources thus creating a vicious feedback loop that both results in failed hydropower investments from missed operational targets, as well as further compounding of the overall physical climate crisis from unplanned emissions.

Similarly, previous natural catastrophes such as typhoons have been known to adversely impact wind farms and floating solar in Japan, raising doubts about the scalability and reliability of these solutions as a viable alternative to traditional energy sources.

A more subtle, but no less disruptive link manifests in general public attitudes towards physical climate risk as more and more people begin to either experience climate catastrophes first hand for the first-time, or are gaining awareness that it is happening to them through advances in extreme climate event attribution science.

Research already suggests that residents in Western Europe who have endured acute risk events, such as heat waves and floods are more likely to vote for Green parties (see the success of the Green party in the German Federal Elections after the floods in Western Germany).

Other more recent but less well-researched and documented instances include Japan’s sudden adoption of the Net Zero Commitment following a spate of highly damaging Typhoons that struck major cities of Osaka and Tokyo across 2018- 2019 – particularly with the unprecedented rainfall following Typhoon Hagibis. For a country that generally eschews sudden and radical policy changes, this is highly significant as Japan is very much dependent on imported fossil fuel energy for domestic energy security, including its key manufacturing sector.

Another notable example is the case of the 2022 Australian Federal Elections following the unprecedented 2019-2020 bushfires and series of severe and widespread East Coast floods, where long-standing conservative stronghold seats fell to ‘teal independents’ campaigning for greater climate action.

As a result, its incumbent climate laggard government was summarily replaced by another with more ambitious climate goals, and, with it greater transition risk to entities that were ill-prepared for such a sudden shift in climate policy.

With political commentators observing that the upcoming NZ election (at the time of writing) will feature climate at the very top of the agenda following the ravaging Auckland floods and ensuing Cyclone Gabrielle, it is likely that this trend of lived climate disaster experiences will accelerate transition pathways beyond smooth trajectories in an increasing number of different jurisdictions.

So, what’s next?

Due to significant uncertainty in climate projections, limitations of current methodologies, and myopic view restricted to financial impacts (our proverbial ‘red herring’), there is a risk of being lulled into a collective false sense of security, resulting in either poor policy decisions or deprioritising further investigative attempts. Instead, by virtue of is irreversible nature, and given what is at ultimately at stake, it would instead be prudent to guard against ‘death by a thousand bites’ by the climate piranha by considering the following:

- A clearer separation between climate stress tests and scenario analysis. Regulators should make exercises more prescriptive to enable comparability across financial institutions – acknowledging that there is still value despite being measured by the same flawed yardstick – but with organisations encouraged to develop their own internal view of risk;

- Broadening the sphere focus of climate scenarios beyond strictly financial outcomes – such as consideration of revenues – in order to not miss ‘early warning signals’ of impending financial stress and promote commensurate mitigative action;

- Ensuring there is representation from various disciplines (i.e., scientists, energy and policy experts, business experts) beyond the status quo of assuming that it lies within the remit of stress testing or risk management.

- Fostering a culture of open debate amongst practitioners – climate scenario analysis is far from settled science, especially beyond academic circles, and contrarian opinions on both sides should be further pondered upon rather than discarded ab initio.

As climate scenario analysis within the broader industry emerges as a discipline, it is critical to ensure that it is not reduced into a compliance driven, ‘tick the box’ exercise with the aim of providing a single loss figure for risk management to fixate upon, and assume will only be relevant to inform capital considerations.

Rather, climate scenario analysis should involve real creativity and an acceptance that a well-constructed analysis should ask more questions to help steer strategic conversations about the financial sector’s role in tackling climate change.

Credits to Prof. Andy Pitman for useful edits, and Insights Artist for support with infographics. All opinions expressed are solely that of the authors.

This article was originally published in UNSW News and has been republished here with the permission of the authors and the UNSW News Team. You can view the original article here.

CPD: Actuaries Institute Members can claim two CPD points for every hour of reading articles on Actuaries Digital.