A new Actuaries Institute Green Paper launched this week, spotlighting serious affordability and transparency issues that are threatening Australia’s private health insurance (PHI) sector.

The Paper “How to make private health insurance healthier” launched on Monday 3 June 2019 at the Actuaries Summit in Sydney. The Summit was attended by more than 560 delegates, including actuaries, insurance and risk professionals, and members of the press.

The Paper called out key industry challenges of:

high and often unexpected out-of-pocket costs for holders of PHI;

a lack of transparency around specialists’ fees and patient outcomes;

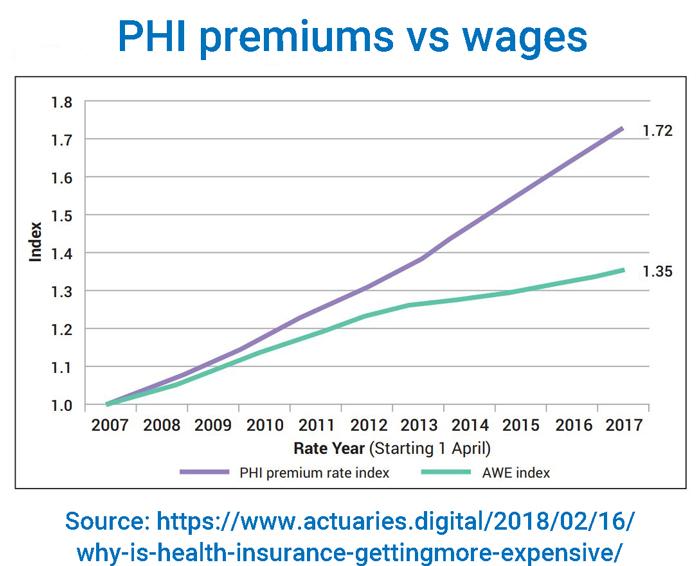

continued declining affordability of PHI; and consequently

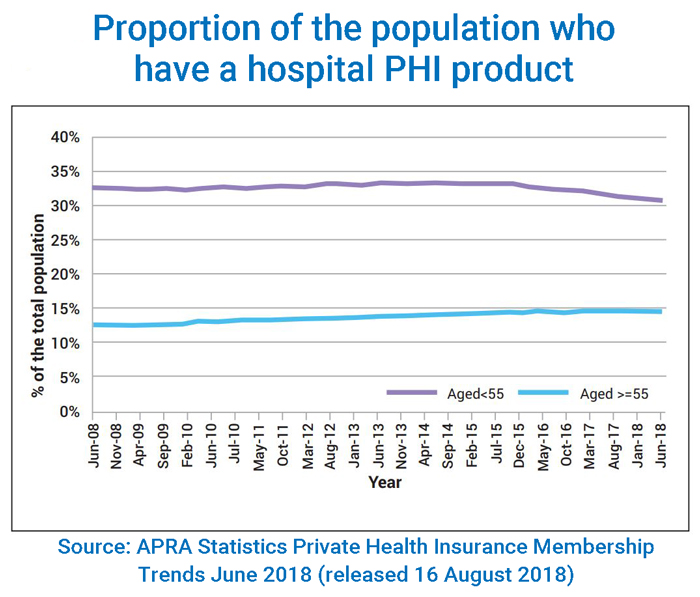

a steady decline in hospital cover participation in recent years.

The challenge of affordability is compounded by community rating, which requires everyone to pay the same price for the same product. This means that the healthiest people with the lowest incomes (a group heavily skewed towards younger generations) are the ones most likely to drop their cover when prices increase.

On average, older (aged 55+) members claim 3.3 times the amount that younger members claim on like for like products. Therefore, the reduction in the participation of younger members puts additional pressure on premiums for the remaining insured population.

It is natural to wonder at what point does this make PHI, in its present form, difficult to sustain?

But actuaries never just wonder, they help find solutions through diligent gathering of a strong evidence base.

Bevan Damm, co-author of the PHI Green Paper speaking at the Actuaries Summit 2019.

Listen to the Podcast where the Paper Authors sat down with Practice Excellence Adviser at the Institute, Vanessa Beenders, to discuss their research and findings.

The Green Paper

The Green Paper was commissioned by the Institute. We prepared the Paper over the course of a number of months, building on our vast experience in the sector, extensive consultation with a wide range of stakeholders, and guided by a Steering Group of senior health actuaries.

The important result of this process is that we have put forward potential solutions that we strongly believe are worthy of exploring by policy makers.

Importantly, in PHI there does not appear to be any single silver bullet solution.

What will be required is a highly collaborative process across multiple stakeholders and a suite of reforms to make PHI healthier.

Matthew and Bevan joined Nick Stolk for a Q&A session during the 2019 Summit.

The key opportunity is to improve transparency by increasing publicly available information around out-of-pocket costs in combination with patient health outcomes from different treatments.

This could empower individuals to make the best choices for their personal circumstances.

Call for independent healthcare coordinators

The Green Paper also calls on policy makers to consider the introduction of independent healthcare coordinators who are paid to help patients navigate the best treatment options and manage the level of out-of-pocket expenses for surgery. This role could be fulfilled by general practitioners, although it would involve additional funding, upskilling and access to relevant data.

A new opportunity for risk equalisation reform

Risk equalisation is the mechanism that supports community rating by sharing claims from riskier members between insurers. However, because it works retrospectively, it means that improved claims efficiencies are also shared, which disincentivises insurers from investing in initiatives to drive these.

A potential solution would be changing risk equalisation to work on a prospective, rather than retrospective, basis. The time has come for this to be back on the table now that standardised product classifications (Gold, Silver, Bronze and Basic) are embedded. These product classifications create natural product ‘floors’ for sharing risks. Such an approach would provide incentives for insurers to drive down claims costs by improving the efficiency and value of the health care services covered (and without compromising cover). Those benefits would be passed to their members in the short term and spread to the community in the medium term through reduced premiums.

Matt Crane, co-author of the PHI Green Paper speaking at the Actuaries Summit 2019.

Improving claims efficiency

Tackling the affordability challenge also requires serious investigation and effort to improve claims efficiency in ways that support policyholders. Health insurance premiums directly reflect the total cost of health insurance claims, which includes a volume of claims element as well as the average cost per claim.

The best way to reduce the volume of claims would be to get everybody healthier, which obviously has broader benefits. Government and private organisations have a shared responsibility to continue to innovate and find new and better ways to drive health improvements.

On the cost side, there are plenty of parts of the supply chain where opportunities lie, for example:

insurers could be more active in promoting, or only supporting, clinically proven treatments;

further reform of prostheses pricing so private health insurers do not face the current 2-5x higher costs compared with the public system; and

reviewing administration fees, which apply in 11% of cases.

Setting a single cost for a treatment pathway

Combining all costs associated with a healthcare treatment pathway into a single total cost, while inherently challenging in the private healthcare industry, is another part of the potential solution and would be a game changer. This would put further pressure on inefficiencies, as the many component costs of a pathway would be set in relation to the overall cost. It would also help patients understand the total cost of their treatments.

Call for action

As recently highlighted by APRA, insurers can do more to ensure a more sustainable industry. In particular, insurers need to offer products that are understood and valued by all of their members, especially younger and healthier members.

However, for reforms to be meaningful and long-lasting, there will need to be collaboration between insurers, medical professionals, hospitals and government.

As with any reforms, there will be winners and losers but driving a high quality and efficient healthcare system needs to be the ultimate objective.

Actuaries encourage the multiple stakeholders to work towards that objective.